The Dilemma: To Buy Now or Wait for Lower Interest Rates in 2025?

The Dilemma: To Buy Now or Wait for Lower Interest Rates in 2025?

The Dilemma: To Buy Now or Wait for Lower Interest Rates?

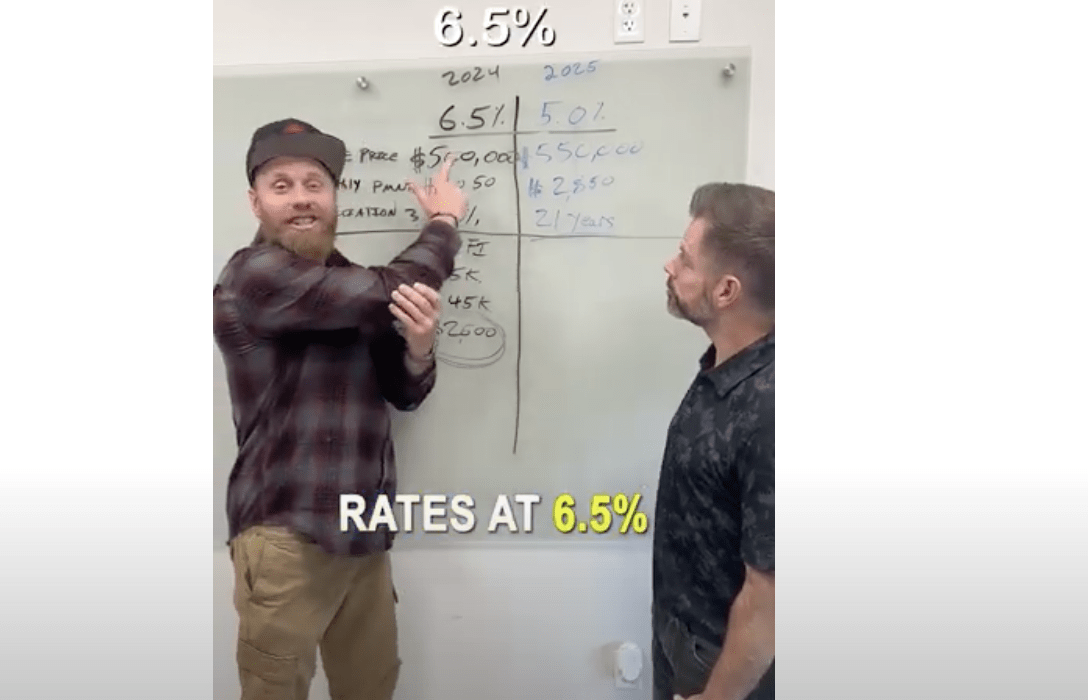

In today’s rapidly changing real estate market, potential homeowners are faced with a critical decision: to buy now at current interest rates or wait, hoping for a decrease. With current interest rates at 6.5% and the anticipation of a drop to 5% by the end of next year, the question looms large. Let’s dive into the numbers to see what makes the most financial sense.

The Current Market: 2024 Scenario

Assuming you’re eyeing a home priced at $500,000 in 2024, with the current interest rates at 6.5%, it’s crucial to understand how this compares with the projected market conditions in 2025. Expectations suggest a 3 to 5% increase in home prices, potentially inflating the cost to $550,000. Additionally, a drop in interest rates is likely to further increase demand, pushing prices up even more.

Today’s Purchase Scenario

Purchasing a home today at $500,000 with a 6.5% interest rate results in a monthly mortgage payment of approximately $3,150. It’s a significant financial commitment, but it’s important to look at the long-term implications.

The Wait-and-See Approach: 2025 Scenario

If you decide to wait until next year, hoping for the interest rate to decrease to 5%, you might be facing a higher purchase price of $550,000 due to market dynamics. The lower interest rate would bring your monthly payment down to around $2,850. At first glance, this seems like a more attractive offer. However, the higher initial cost of the property means that it would take 21 years of lower payments to offset the additional $50,000 spent on the home’s purchase price.

The Refinancing Factor

Another angle to consider is refinancing your mortgage when the interest rates hit 5%. Refinancing could lower your monthly payment to $2,600, even after accounting for the approximate $5,000 cost of refinancing. This strategy puts you $45,000 ahead in terms of property value, with the added benefit of reduced monthly payments.

Making the Decision

The decision to buy now or wait hinges on several factors. Paying an extra $200 per month for 12 months could essentially “earn” you $50,000 in home value if prices rise as expected. This calculation doesn’t even account for the potential savings from refinancing to a lower rate in the future.

Call or Text me now to go over your situation.

-Justin Critchfield 801-891-5489

Team Plus Realty

Broker